Have questions about Arizona Medicare? Let us help you make the right decision. Discover local tips and answers to your frequently asked questions in this ultimate guide.

Speak with a local licensed insurance agent:

(623) 223-8884 (TTY: 711) M-F 9am - 5pmMedicare is a federal health insurance program that provides access to healthcare services and helps reduce the cost of care for millions of eligible individuals across America.

Medicare is a federally-regulated system administered by the Centers for Medicare & Medicaid (CMS). Regardless of your state, this program ensures citizens across America access quality healthcare services.

In 2023, over 1.4 million (1,437,788) Arizona residents (7,379,346) are enrolled in Medicare. That’s nearly 20% of Arizonans. If you’re Medicare-eligible or aging in, you’re in good company.

Continue reading to learn if you’re eligible for Medicare in Arizona.

What makes you eligible for Medicare in Arizona? Either your age or a disability approved by the Social Security Administration.

Are you looking for affordable healthcare options in Arizona? You might be eligible to apply for Medicare if one of the following applies to you:

Are you a senior, a person with disabilities, or someone who has had ESRD (End-Stage Renal Disease)? If so, then Medicare may be right for you.

Now that your eligibility is checked off the list, it’s time to learn about your Medicare plan options in Arizona. Continue reading to learn which plan may be best for your health and budget.

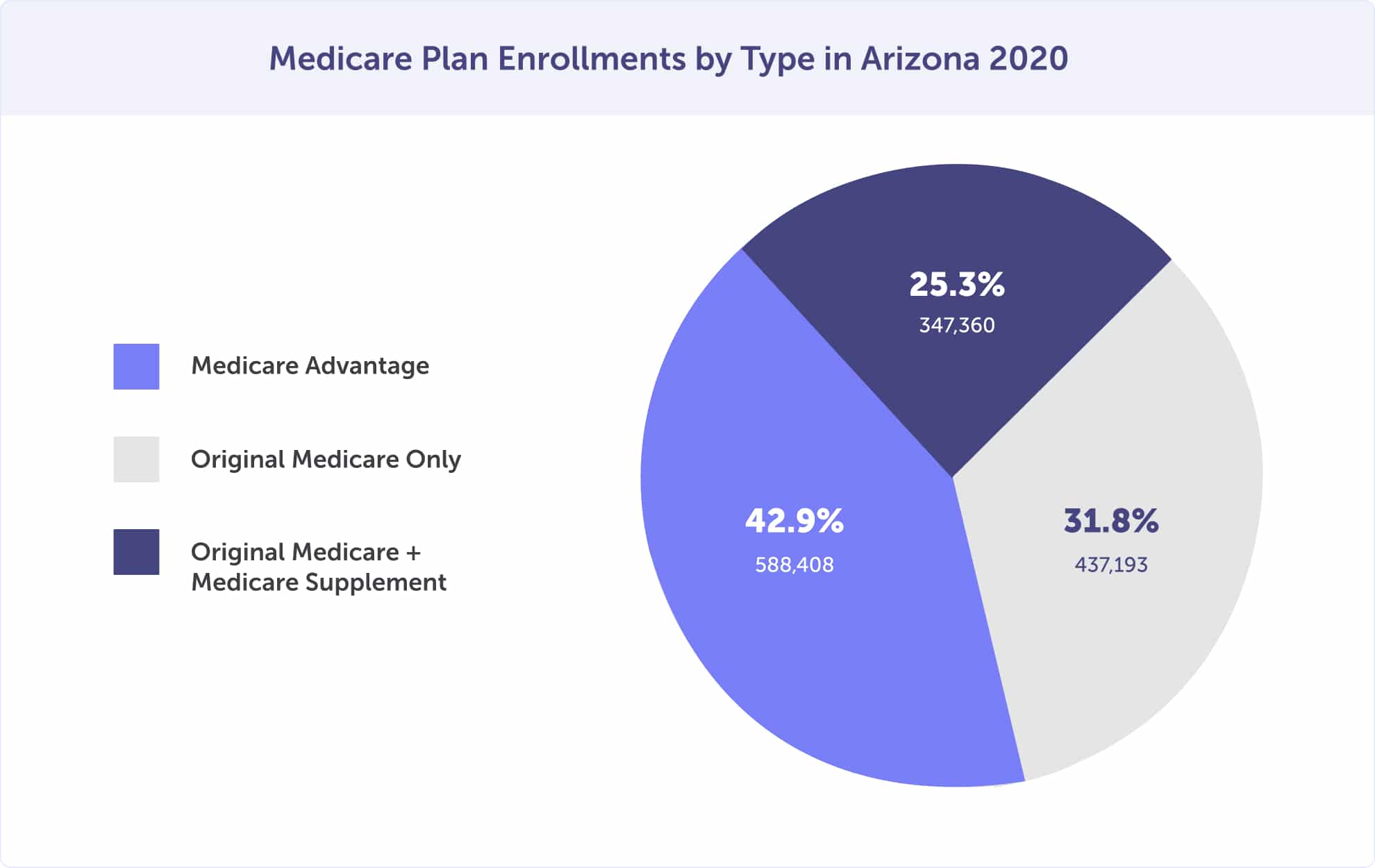

Of the 1.4 million Arizonans enrolled in Medicare, 24% (347,360) are enrolled in Original Medicare Part A and B plus a Medicare Supplement plan. And 42% (588,408) of Arizonans are enrolled in a Medicare Advantage plan.

Combined, 66% of beneficiaries are enrolled in a plan that shields them from high or surprise out-of-pocket costs they can be expected with Original Medicare alone.

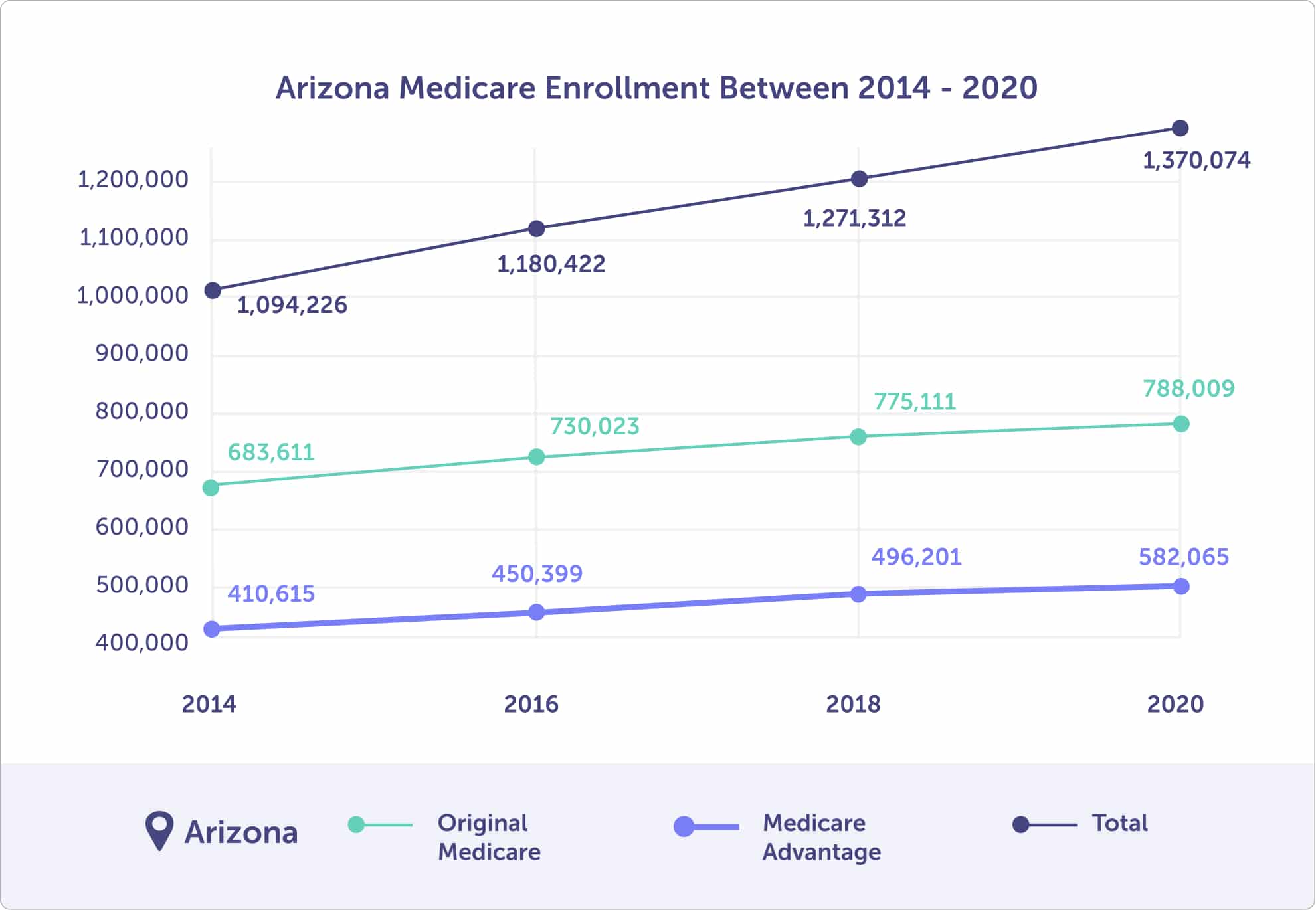

Arizonans enrolled in a Medicare Advantage plan have increased by 5%, from 38% (410,615) in 2014 to 43% (582,065) in 2020.

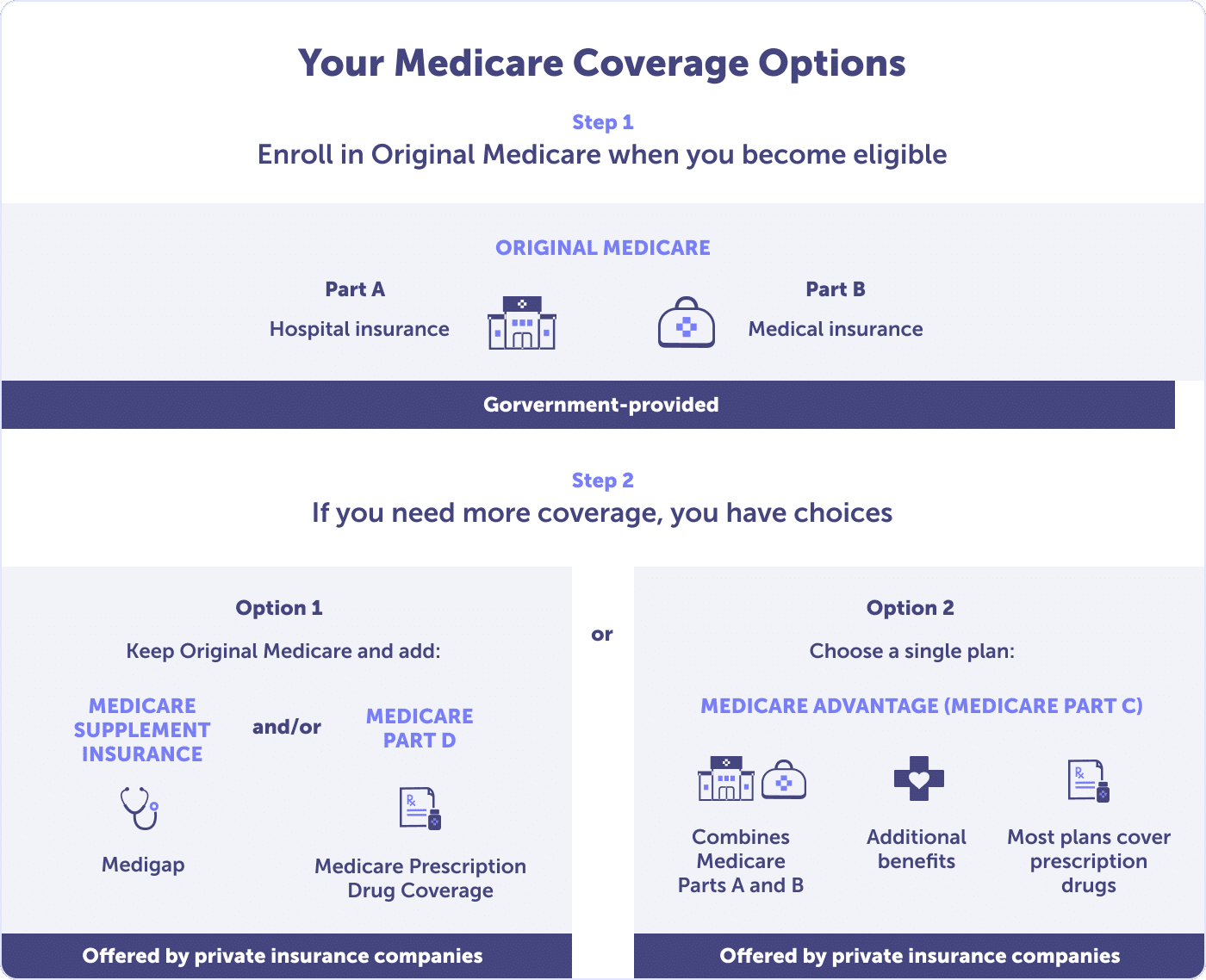

While exploring the world of Medicare, you’ll find yourself at a crossroads, faced with two options that will decide your healthcare future.

1. Enroll in Medicare Parts A and B (Original Medicare), plus stand-alone prescription drug coverage (Medicare Part D) and, likely, a Medigap plan (Medicare Supplement).

OR

2. Enroll in a Medicare Advantage Prescription Drug Plan that includes Medicare Parts A and B coverage, prescription drug coverage, and additional benefits. Or a Medicare Advantage Plan that doesn’t have prescription drug coverage (Medicare Part C) but does offer benefits like vision, dental, and hearing coverage.

Everyone should enroll in Original Medicare Parts A & B. Once enrolled, tackle those pesky out-of-pocket expenses. Consider joining the 66% of Arizonans who wisely opted for a Medicare Advantage or Medicare Supplement plan – protecting themselves from the high out-of-pocket costs that Original Medicare can expose you to.

Ready to uncover the perfect mix for your healthcare and budget needs? Explore Medicare Parts A, B, C, and D plus Medicare Supplement plans – our team is here to help you find an excellent fit.

Medicare Part A (hospital insurance) is part of Original Medicare. Part A is the public option the federal government provides. The best part? It’s usually premium-free.

Medicare Advantage plans also provide coverage for Medicare Part A. Because they are contracted with the Centers for Medicare & Medicaid Services (CMS), this is a requirement.

Meet one of these criteria to be eligible for Original Medicare Part A in Arizona:

Medicare Part A is your public hospital insurance. Part A covers medically-necessary hospital services provided in a Medicare-approved facility by a Medicare-assigned provider.

These services include:

Medicare Part A has coverage limitations. Uncover the exclusions and protect yourself from unexpected expenses. Read more about Medicare Part A.

Your Medicare Part A will likely be premium-free if you meet specific criteria.

In Arizona, you must be at least 65 or older and:

Are you under 65 years of age? You may receive premium-free Part A if you:

Don’t worry if you and your spouse don’t qualify for premium-free Part A healthcare coverage. You still have the option to purchase it; in 2026, the cost could be up to $565 monthly.

Ready to know the mystery behind your Medicare Part A premium costs? It’s all in the quarters.

If your contributions span less than 30 quarters, you’ll have a monthly premium of $565. But, those who’ve paid Medicare taxes for 30 to 39 quarters get a deal: their premium drops to $311 a month.

When you purchase Medicare Part A, you must also purchase Part B medical insurance. Then, you’ll pay your Part A and Part B premiums. However, if you choose not to buy Part A, you can still purchase Medicare Part B.

Medicare Part A expenses go beyond premiums. Whether you pay a premium or not, include Part A deductibles, coinsurance, and copays in your healthcare budget.

In 2026, the Medicare Part A deductible is $1,736.

If you’re receiving inpatient care, your coinsurance costs could vary depending on how long your stay is. The amount owed increases with each day – so if it’s possible to be discharged sooner rather than later, do what you can.

In 2026, Medicare Part A coinsurance is:

Curious about what it would cost if you need inpatient care? If you receive care for about five months (150 days), you could owe about $62,850 in coinsurance.

The table below shows the breakdown of coinsurance cost by days – and what you could pay with Original Medicare alone.

2025 Potential Cost of 1 - 150 Days of Inpatient Care

Your coinsurance costs, plus the deductible, could be higher than $62,850. Keep in mind Medicare Part A covers only Medicare-approved expenses.

But what if you have an inpatient stay beyond 150 days? That would be out-of-pocket.

That’s why 66% of Arizonans enroll in a Medicare Advantage or Medicare Supplement plan. A Medicare Advantage plan caps your out-of-pocket expenses, while a Medicare Supplement plan can help pay for some or all of them.

If you have a service performed that wasn’t Medicare-approved, that would also be out-of-pocket. That is why knowing what Medicare does and doesn’t cover is crucial. And that you get pre-approval in some cases. To prevent surprise or high costs, read more about Medicare Part A.

Enrolling during your Initial Enrollment Period is the ideal time to sign up for Medicare Part A. However, you can still sign up later if needed — the General or a Special Enrollment Period if you qualify.

Medicare Part A provides hospital insurance, while Medicare Part B provides medical insurance. Medicare Part B is the second part – and the complement that completes Original Medicare.

You may enroll in Part B in Arizona if eligible for Orignal Medicare Part A. That means you must qualify through one of the following:

Original Medicare Part B covers medically necessary and preventative services.

Original Medicare Part B covers:

Want a comprehensive list of what Medicare Part B covers? Check Medicare’s What Part B covers.

Medicare Part B’s standard premium for 2026 is $202.90. This is the standard premium because it’s the minimum most people pay. However, the Part B premium is based on income, so you may pay more.

Medicare Part B’s premium is adjusted for your individual or joint modified adjusted gross income. While most people pay the standard premium, you could pay higher if you made more than a specific threshold. In 2026, you could pay the standard $202.90 premium plus an Income Related Monthly Adjustment Amount (IRMAA).

Here’s where it gets a little tricky. The Centers for Medicare and Medicaid Services (CMS) bases your premium on the modified adjusted gross income reported to the IRS two years ago. For 2026, the Part B premium amount is based on the federal tax return from 2024.

Find your 2024 modified adjusted gross income below to see if you’ll pay an IRMAA in 2026. Or read more about Medicare Part B costs.

2026 Medicare Part B Premium & Income Related Monthly Adjustment Amount (IRMAA)

In 2026, Arizona’s Medicare Part B deductible is $283.

Once the $283 deductible is paid for the year, typically, you pay a 20% coinsurance for Medicare-approved services after that point. That’s 20% for doctors’ services when you’re checked into a hospital, for outpatient therapy, Durable Medical Equipment (DME), and more.

It’s critical that you know that Original Medicare Part A and B do not cap out-of-pocket costs. That means you will pay 20% for every Medicare-approved service unless you are enrolled in a plan that expands your Original Medicare coverage.

A Medicare Supplement plan can help you pay for some or all of your Medicare-approved costs, while a Medicare Advantage plan can reduce out-of-pocket costs because they cap out-of-pocket expenses.

Preventative services under Medicare Part B are typically free from a healthcare provider that accepts Medicare and doesn’t require a 20% coinsurance cost.

Concerns about whether a test, item, or service is covered by Original Medicare? Medicare has a helpful tool that lets you know if it’s covered.

But remember, some services and tests require pre-approval. If you are admitted, we recommend requesting hospital orders to avoid costly out-of-pocket or surprise bills. We recommend you also negotiate the cost of services before they are provided.

When is the best time to enroll in Medicare Part B? During your Initial Enrollment Period. But if you miss your Initial Enrollment Period, you still have a chance to enroll – but at a cost. The next best opportunities are the General Enrollment Period or, if you qualify, a Special Enrollment Period.

You’ll likely face lifetime late enrollment penalties if you miss your Initial Enrollment Period and enroll during the General or a Special Enrollment Period.

You have the option to delay Medicare Part B enrollment. But if you do, you must have the equivalent of Part B coverage from another source. This is called creditable coverage.

Every year you should receive a Notice of Creditable Coverage should you receive Part B equivalent coverage from:

Ensure that you maintain creditable coverage until you enroll in Medicare Part B. This will ensure that you avoid lifetime late enrollment penalties.

Discover the benefits of Arizona’s Medicare Advantage plans or Medicare Part C. These dynamic plans, provided by private insurers and overseen by the Centers for Medicare & Medicaid Services (CMS), bring added benefits to Medicare coverage, ensuring your healthcare needs are met with extra benefits.

Medicare Advantage plans have a maximum for out-of-pocket expenses, unlike Medicare. Want a Medicare Advantage plan that includes creditable prescription coverage? Then you should enroll in a Medicare Advantage Prescription Drug Plan.

You should begin your Medicare Advantage plan journey by enrolling in Medicare Part A and B. Then, you can choose a Medicare Advantage plan based on the area where you live. Medicare Advantage plans are offered at the county level, and many options are available.

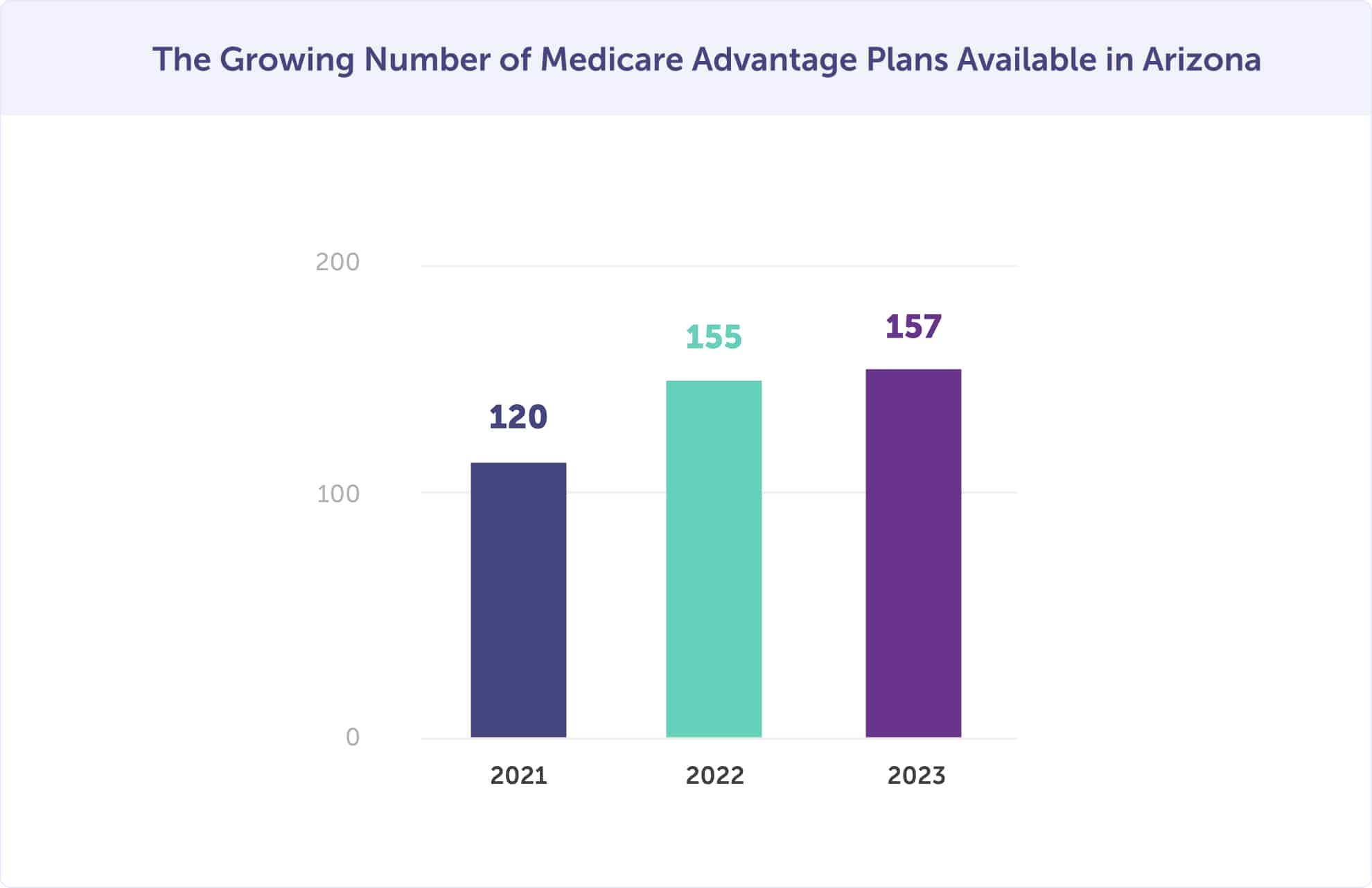

In 2026, there are 157 plans in Arizona. But you will only have a portion of these available because they’re not accessible in every county.

The number of plans available in 2026 is up only slightly compared to 2022 when there were 155 plans available.

However, between 2021 and 2022, there was a 29.2% increase in Medicare Advantage plans. Jumping from 120 to 155. In 2023, 49.5% of Arizonans are enrolled in a Medicare Advantage plan.

It’s good that there are more plans available each year. This means that when you comparison shop, you have a greater opportunity to find a plan uniquely suited to your health and budget. It can also mean that more insurance providers offer innovative plans and compete for your choice – giving you the upper hand.

While Medicare Advantage plan options continue to grow year-over-year in Arizona, there are a few counties where the percentage of Medicare recipients are enrolled in a Medicare Advantage plan the most.

In 2026, the five Arizona counties with the most Medicare Advantage plan enrollees are Santa Cruz County (61%), Pima County (57%), Graham County (54%), Maricopa County (51%), and Pinal County (50%).

2023 Top 10 Arizona Counties with the Highest Percentage of Medicare Advantage Enrollment

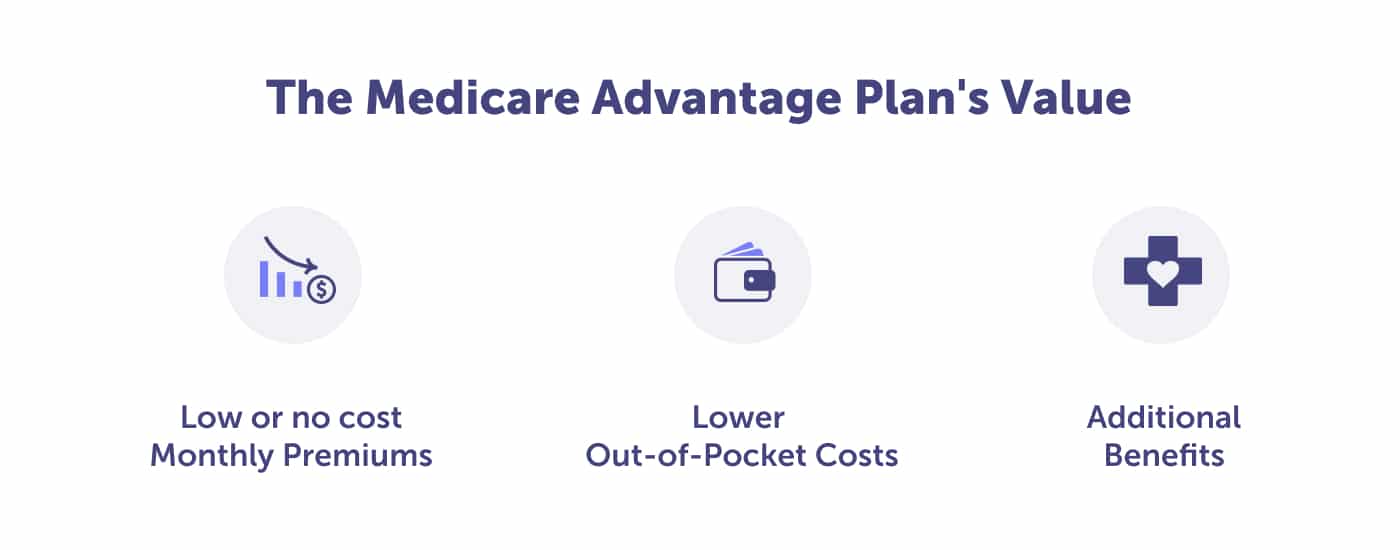

Want low or no-cost premiums and lower out-of-pocket costs? A Medicare Advantage plan can provide that and more. A Medicare Advantage plan offers equivalent coverage to Part A and B, often at a lower price, plus additional benefits that Original Medicare doesn’t provide. It’s clear why nearly 50% of Arizonans are enrolled in a Medicare Advantage plan.

Are you enrolled in Medicare Parts A & B in Arizona? Then you have access to a $0 monthly premium Medicare Advantage plan. For those who don’t enroll in a $0 premium Medicare Advantage plan, the average premium is $12.00.

Once you enroll in a Medicare Advantage plan, you’ll continue to pay your Medicare Part A and B premiums, plus any Medicare Advantage plan premium. Another bonus with Medicare Advantage plans – the majority offer prescription drug coverage. That means you don’t have to enroll and pay for a standalone Part D prescription drug plan.

It’s hard to believe that Original Medicare has no cap on out-of-pocket costs. That means you could spend an unlimited amount on copayments and coinsurance. Those costs could be substantial since the 20% Original Medicare coinsurance has no cap.

Medicare Advantage plans are different. These plans set their deductibles, coinsurance, and copayments within limits set by the federal government. With limits, you’ll know what your highest financial liability could be.

Medicare Advantage plans provide peace of mind because once your plan’s out-of-pocket maximum is reached, including deductible, your plan pays 100% of covered healthcare expenses for the remainder of the plan year.

Original Medicare does not cover comprehensive dental, vision, and hearing coverage. Suppose you want to visit the dentist with Original Medicare; that would be out-of-pocket.

If you’d like to see a dentist, optometrist, or audiologist for routine care, you should enroll in a Medicare Advantage plan. These are just the basics. Medicare Advantage plans cover so much more than Original Medicare.

Most Medicare Advantage plans include reduced cost-sharing, over-the-counter and wellness products, transportation help, telemedicine, a gym membership, and other rewards and incentive programs.

There is a unique program that the Centers for Medicare and Medicaid Services (CMS) Innovation Center’s Value-Based Insurance Design (VBID) offers in Arizona.

Thirty plans offer Medicare Advantage enrollees eliminated Part D cost-sharing, rewards, incentive programs for healthy behaviors, benefits for underserved and/or chronically ill enrollees, and benefits that address food insecurity and social isolation.

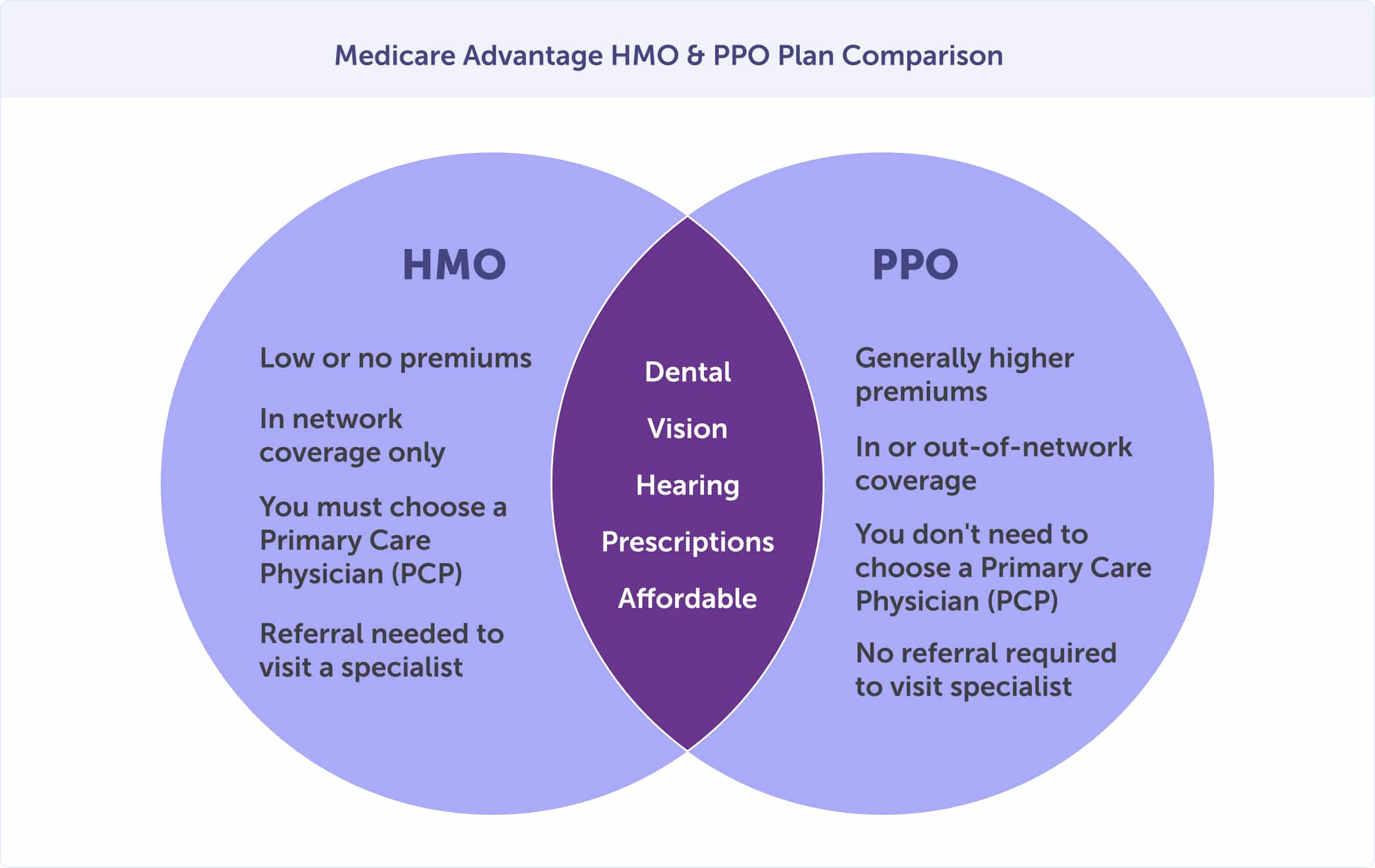

While four Medicare Advantage types are available in Arizona, two are the most popular. Health Maintenance Organizations (HMOs) and Preferred Provider Organizations (PPOs) are the most popular.

Special Needs Plans (SNPs) and Private Fee-for-Service (PFFS) plans have lower enrollment but are still good options if they’re available and fit your health and budget needs.

When choosing your Medicare Advantage plan, you’ll likely choose between an HMO or PPO plan. PFFS plans are available in predominantly rural areas.

HMO and PPO plans provide different network flexibility and price levels, which you’ll be weighing when choosing.

What do Medicare Advantage HMO, PPO, SNP, and PFFS plans have in common?

Medicare Advantage HMO and PPO plans also have several commonalities.

What is the main difference between HMO and PPO plan type options? Ultimately, you’ll be weighing cost and flexibility.

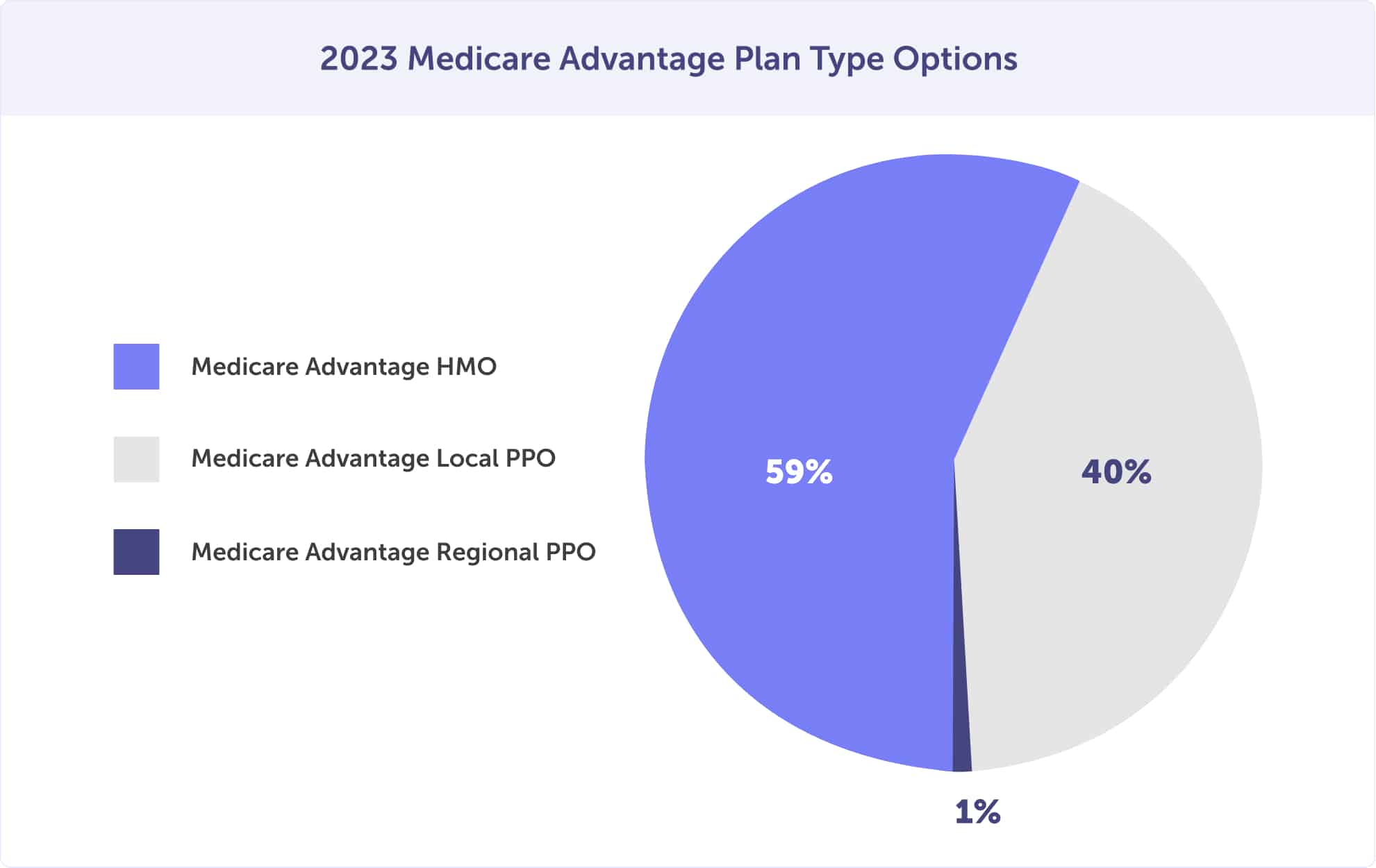

In 2023, most Medicare Advantage plan enrollees had an HMO (59%), while 40% enrolled in a local PPO. The least popular option was the regional PPO plan option – with 1% enrollment.

The Centers for Medicare & Medicaid Services (CMS) requires that Medicare enrollees have creditable prescription drug coverage. You can receive this coverage through a Medicare Advantage plan. When traditional Medicare Part C and prescription drug coverage are paired, that’s called a Medicare Advantage Prescription Drug plan.

Want the convenience of one card and plan that covers all your Medicare needs? A Medicare Advantage plan is the best choice. These plans cover your hospital, medical, and prescription drugs in one plan. A Medicare Advantage plan can help you avoid an additional Part D prescription drug plan premium.

Most Medicare Advantage plans offer a Medicare Advantage Prescription Drug plan (prescription drug coverage). In fact, in 2020, 90% of the plans provided MAPDs, and 89% of all Medicare Advantage enrollees were enrolled in an MAPD plan.

14 Medicare Advantage Plan Providers in Arizona

Want a $0 premium Medicare Advantage plan? You’re in luck. Everyone enrolled in Medicare Part A and B can access a Medicare Advantage plan in Arizona with a $0 monthly premium. If you choose a plan with a premium, the average monthly cost is $12.00 in 2026.

After enrolling in a Medicare Advantage (traditional Medicare Part C) or a Medicare Advantage Prescription Drug plan that includes prescription drug coverage, you pay your plan premiums directly to the provider. Your Medicare Advantage premiums are separate from your Medicare Part A and B premiums which are paid directly to Medicare.

Your Original Medicare premiums are usually withdrawn from your Social Security benefit, electronic withdrawal, or coupon book. When you enroll in Original Medicare, you can choose your payment method.

In addition to your Medicare Advantage plan premium, you’ll likely have out-of-pocket expenses for deductibles, copayments, and coinsurance. These costs will depend on which plan you choose.

Unsure of the best Medicare Advantage plan for you? You should weigh your coverage and cost options. First, you must decide whether you want an HMO or PPO plan. From there, you can ask yourself a few simple questions to find the right plan for your health and budget.

The best time to enroll in an Arizona Medicare Advantage plan is during your Initial Enrollment Period. Has your Initial Enrollment Period passed? Don’t worry; you can still enroll during the General or Special Enrollment Period if you qualify.

If you enroll in a Medicare Advantage plan and then want to change plans, you can do that during the Medicare Advantage Open Enrollment Period.

Discover Medicare Part D, a federal initiative designed to provide essential prescription drug coverage for those eligible, ensuring consistent access to life-enhancing medications. Part D is offered through privately-regulated insurance firms and supervised by the Centers for Medicare & Medicaid Services (CMS) – similar to Medicare Advantage plans.

Most enrollees are enrolled in Medicare Part D if enrolled in Original Medicare alone, but not if they are enrolled in Medicare Part C.

Enrollees get coverage from a Medicare Advantage Prescription Drug Plan to get prescription drug coverage with a Medicare Advantage plan. When making enrollment decisions, you’ll need to choose a Medicare Advantage Prescription Drug plan or a Medicare Part D plan, but you can’t have both.

Medicare Part D helps beneficiaries pay for some of the costs of prescription drugs at participating pharmacies. The availability and cost of plans vary by county. Part D typically has a monthly premium, depending on your plan choice, plus an annual deductible, copayment, and/or coinsurance.

In 2026, 28 stand-alone Medicare Part D prescription drug plans are available in Arizona. Of those enrolled in Medicare Part D in Arizona, 25% receive Extra Help (the Low-Income Subsidy).

What is Medicare Part D Creditable Coverage?

Don’t let penalties haunt your Medicare journey. Be prepared with creditable prescription drug coverage, as mandated by the Centers for Medicare & Medicaid Services (CMS).

Avoid the penalties by enrolling in either a Medicare Advantage Prescription Drug plan. Or a standalone Medicare Part D prescription drug plan paired with your Original Medicare Parts A and B.

Another option is to have creditable coverage from another source, like an employer. That creditable coverage source would need to provide proof that their coverage is equal to the coverage of Medicare Part D.

You could receive creditable coverage from a source such as:

If you ever lose your creditable coverage or group health insurance, you must enroll in Medicare Part D or a Medicare Advantage Prescription Drug plan within 63 days of losing coverage. And if you don’t? You can expect to pay late enrollment penalties when you do.

If enrolled in Original Medicare Part A and/or Part B, you can access a Medicare Part D prescription drug plan in Arizona.

Every plan has a formulary, which is a unique list of prescription medications that are covered. Be careful in your choice because every plan is different, and plans do not cover the same medications. You should check the formulary for any brand-name, generic, or protected-class drugs that you need are available. Protected class medications include treatment for HIV/AIDS and cancer, among others.

Worried that your prescription might not be on the formulary? There’s good news. The Centers for Medicare & Medicaid require each Medicare Part D formulary to have at least two drugs in the most commonly prescribed categories and classes. This requirement allows people with common prescriptions to get the medicine they depend on.

And, if the formulary for your plan doesn’t include your prescription, a brand name, for example, a similar medication, should be available. If there isn’t a substitute, you can always request an exception.

Just like Medicare Advantage and Medicare Supplement plans, Medicare Part D plans change annually. We recommend you review your plan annually during the Annual Enrollment Period, October 15 – December 7.

Reviewing your plan can help in several ways:

Without a Medicare Part D plan review, you may miss out on savings or face higher prescription drug costs. Worse yet, you may enter the new year not knowing your prescription is unavailable. You don’t want any of these scenarios to happen to you.

Arizona’s lowest monthly premium for a standalone Medicare Part D prescription drug plan in Arizona is $5.40. In 2026, the national average monthly premium for standard Medicare Part D prescription drug coverage is $36.78.

Aside from the monthly premium, there are other Medicare Part D costs. The plan you choose will also have out-of-pocket costs. These expenses include the annual deductible and copayment, and/or coinsurance.

You should check the plan’s formulary to know how much a prescription refill might cost. Plan formularies have levels of coverage called “tiers.” The higher the tier, the higher medication’s cost. A generic medicine is usually a lower-tier prescription. If you choose a generic version, you’ll save money.

Don’t worry about the quality of generic medication. They are not of lesser quality. Instead, the Food and Drug Administration (FDA) requires generic drugs to be copies of brand-name drugs.

Generics must be the same in dosage, safety, strength, administration, quality, performance, and intended use. To save money, consult your doctor or prescriber about generic drug options.

Your Medicare Part D deductible will depend on the plan you choose. In fact, some Part D plans don’t even have a deductible. However, those plans that do can be no higher than $590 in 2026.

There is Medicare Part D extra help if you have limited financial resources and income. If you need help and you’re enrolled in Arizona Medicare, you should see if you qualify for Extra Help.

The Low Income Subsidy, or Extra Help, can help you pay your monthly premiums, annual deductible, and Medicare Part D prescription co-payments.

A bonus if you’re eligible for Extra Help – you won’t receive a late enrollment penalty when joining a Medicare drug plan.

Every year, the Centers for Medicare & Medicaid Services (CMS) provides Star Rating for each Medicare plan. The CMS Star Rating system can help you gauge what you might expect from a plan’s customer service, preventative care, the management of chronic conditions, responsiveness, and if there were member complaints. The ratings are on a scale of 1 to 5, with 4 and 5-star ratings being excellent.

There are no 5-star rated Medicare Part D plans in Arizona. The highest-rated plan is UnitedHealthcare’s AARP MedicareRx Preferred (PDP) is the highest-rated plan, which has 3.5 stars. When choosing plans, you may want to consider this highest-rated plan in Arizona.

These insurance carriers offer Medicare Part D stand-alone prescription drug plans in Arizona.

11 Medicare Part D Providers in Arizona

The ideal time to sign up for Medicare Part D is during your Initial Enrollment Period.

Should you miss your IEP, you can still enroll during the General Enrollment Period. The downside? You’ll have late enrollment penalties. You could also enroll during a Special Enrollment Period if you qualify.

Discover the advantages of a Medicare Supplement plan, called a Medigap plan. This exceptional upgrade offers Original Medicare participants the peace of mind of more stable and easily anticipated out-of-pocket expenses.

Medigap plans are not stand-alone plans – they work with Original Medicare. You can rest easy because the Arizona Department of Insurance authorizes and licenses the companies that provide Medigap plans. And plans are standardized, meaning each private insurance company must offer the same coverage level.

When you enroll in Original Medicare Parts A & B with a Medigap plan, you must ensure you also have creditable prescription drug coverage. Medicare Supplement (Medigap) plans do not provide creditable coverage, but you can get that from a stand-alone Medicare Part D plan or another source.

The AHIP’s State of Medicare Supplement Coverage reports that in 2021, 25.1% (351,769) of Medicare-eligible Arizonans purchased a Medicare Supplement plan. That’s down from 25.3% (347,360) in 2020 and 25.6% (340,158) in 2019. Medicare Supplement enrollment is down by 0.2% year-over-year.

If you enroll in only Original Medicare, you’re putting yourself at financial risk. Medicare Part A and B do not have a limit for out-of-pocket expenses. Medicare Part A covers some inpatient costs, and Medicare Part B covers 80% of outpatient expenses. With Original Medicare alone, you’ll still need to pay out-of-pocket for deductibles, copayments, and 20% coinsurance for doctor visits and medical expenses.

These out-of-pocket expenses, and the coverage gap, could cost much more than you expect. For instance, you could be on the hook for the costs of a hospital stay over 60 days or 20 days at a skilled nursing facility. The coinsurance can hurt you financially. That’s where a Medicare Supplement (Medigap) plan can help your peace of mind.

Depending on the plan you choose, a Medicare Supplement plan can help you pay for some or all of the following costs:

Arizona has 10 types of Medicare Supplement plans. The plans are A-G and K-N. Arizona requires that each Medicare insurance company offer Medicare Supplement Plan A at a minimum.

While there are ten types of plans, only some of these will be available to you. That’s because plans that include the Part B deductible have been phased out. If you turned 65 on or before December 31, 1999, you could still enroll in Plan C and F. However, if you turn 65 on January 1, 2020, or later, these two plans are unavailable. Plan J is not taking new enrollments.

The top Medicare Supplement plans in Arizona are Plan F (41.7%), Plan G (34.7%), Plan C (8.3%), and Plan N (7.1%). Of these plans, Plan G and Plan N are rising in enrollment due to the phase-out of Plan C and F.

Top Arizona Medicare Supplement Plans

Be careful not to make your enrollment decisions based on plan popularity. Your plan must be tailored to your unique health and budget needs, which doesn’t necessarily mean the most popular plan is best for you.

Consider your health, plus the monthly premium costs and out-of-pocket expenses. Some plans may have higher out-of-pocket costs but a lower monthly premium. Which is more important to you?

While Medicare Plan F has the highest enrollment in Arizona, it was phased out on January 1, 2020. You could still enroll if you turned 65 on or before December 31, 1999. But if you turned 65 after that date, you’ll need to choose amongst other plan options.

Plan G is the closest to discontinued Plan F, which may be a good alternative. It’s also likely why Medigap Plan G has the second-highest enrollment in Arizona.

51 Medicare Supplement Plan (Medigap) Providers in Arizona

There are three requirements to be able to enroll in a Medicare Supplement Plan. You should be enrolled in Original Medicare Part A and B, plus live in the county where the plan is available.

The best time to enroll in a Medicare Supplement plan in Arizona is when you first become eligible. Your enrollment eligibility is tied to your unique Medigap Open Enrollment Period. This one-time enrollment cannot be changed or repeated, so you must know when it occurs.

Should you miss your Medigap Open Enrollment Period, you may not be able to enroll in a plan. If you want to enroll outside your enrollment period, you will likely need to go under medical underwriting. During your Medigap Open Enrollment Period, you can enroll in a plan regardless of preexisting conditions and not face pricing discrimination.

The Medicare landscape has critical enrollment periods to help you get coverage and benefits. Your Initial Enrollment Period, General Enrollment Period, and Medigap Open Enrollment Period are all key opportunities to apply for Medicare. If your window passes, however, don’t worry – there could still be hope in a Special Enrollment period – if you qualify.

Arizonans become Medicare-eligible when they turn 65. During your Initial Enrollment Period, you get seven months to sign up – three months before that all-important birthday month, your birth month, plus an additional three months. Take advantage of this beneficial opportunity; start planning for it today.

Missing your Initial Enrollment Period could have serious consequences. With late enrollment penalties, you want to avoid waiting for the General Enrollment Period; make sure you enroll during this critical window.

Discover the date of your Initial Enrollment Period and get on track for Medicare with a straightforward quiz. Take our eligibility quiz today, and you’ll know when to enroll and receive helpful reminders – so that nothing slips through in this critical process.

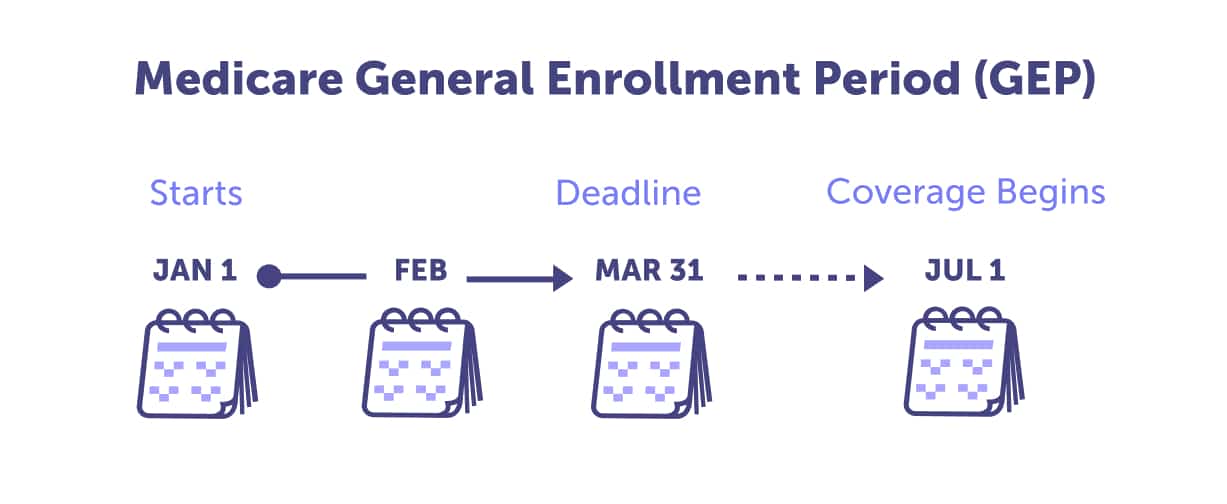

If you miss your Initial Enrollment Period, don’t worry. Every year from January 1 to March 31, you have a second chance with the General Enrollment Period. Those who take advantage will have access to coverage on July 1 – just make sure not to miss it.

Note: If you enroll in Medicare during the General Enrollment Period, you may incur late enrollment penalties.

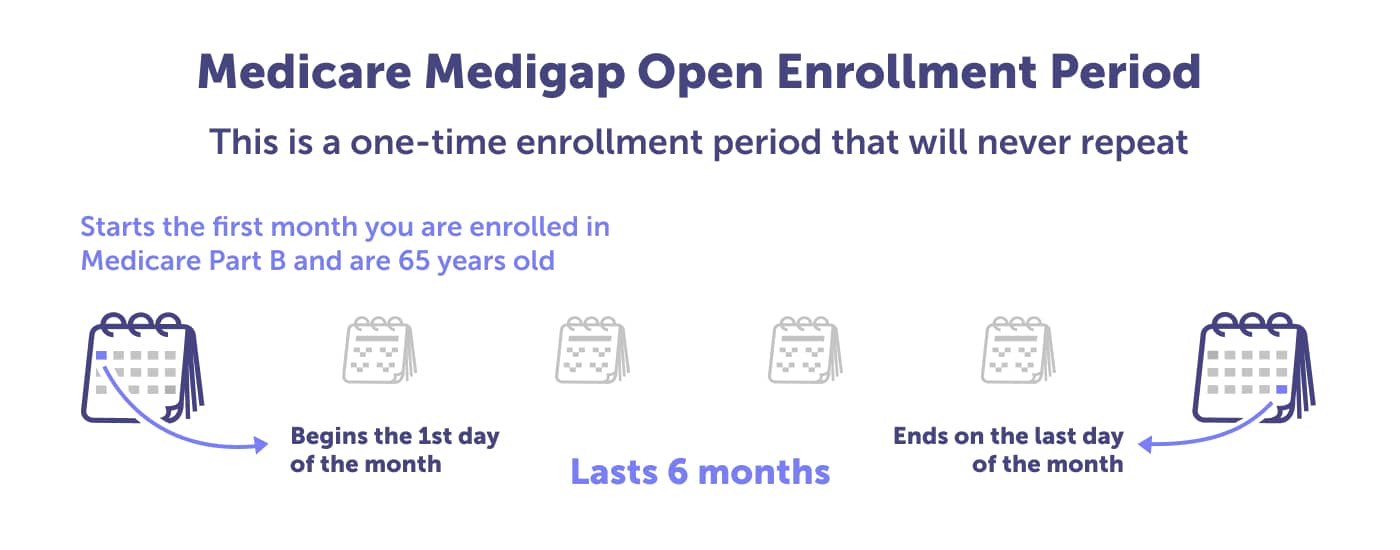

The Medigap Open Enrollment Period is the best time to enroll in a Medigap plan, also called a Medicare Supplement plan. If you’re considering enrolling in a Medicare Supplement plan, mark your calendar for the first month you’re enrolled in Medicare Part B and are age 65. This one-time enrollment period lasts only six months, happens once, and can not be extended or changed.

Your Medigap Open Enrollment Period is optimal for choosing a Medicare Supplement plan. Enrolling during this period lets you quickly find and select from several great plans without worrying about higher costs or medical exclusions. Plus, if you miss your chance – it may be more difficult and expensive. In the future, you could require underwriting and be denied Medigap coverage.

Need Help Deciding The Right Medicare Coverage For You?

![]() No-cost, unbiased service

No-cost, unbiased service![]() Compare all major plans and carriers

Compare all major plans and carriers![]() Local, licensed insurance agents with 25+ years of combined experience

Local, licensed insurance agents with 25+ years of combined experience

Reviewing your coverage and making appropriate adjustments is critical to ensure you have the best health and budget plans. There are three critical times each year when enrollment changes can be made: the Annual Enrollment Period, the Medicare Advantage Open Enrollment Period, and Special Enrollment Periods – make sure not to miss them.

Take advantage of the chance to save money and get better benefits – mark these enrollment periods in your calendar. Taking time to compare plans guarantees that you have an optimal healthcare solution for both your pocketbook and well-being.

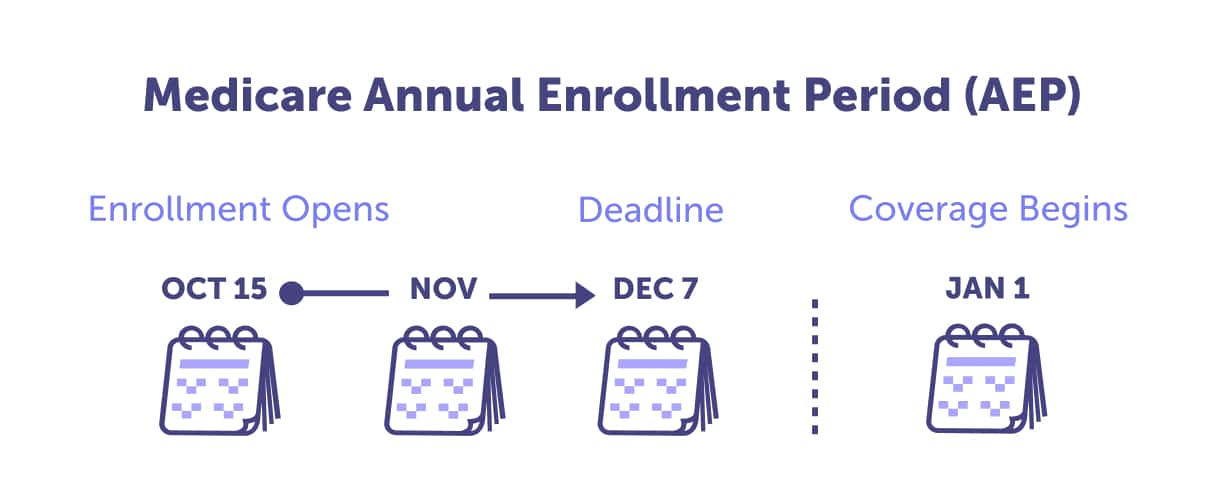

The Annual Enrollment Period (AEP) is when you revisit and review your Medicare plan. The window of opportunity begins October 15th and ends December 7th. If you’re already enrolled in Medicare, this is when you can make any necessary updates or changes to your health coverage for the upcoming year.

The Annual Enrollment Period is when it’s time to examine your coverage closely. Evaluating annually with a local licensed agent helps ensure you get all the health support and savings that are right for you. Why?

Now is the time to be proactive and ensure you’re prepared for Medicare’s Annual Enrollment Period. Check out our guide for helpful advice on maximizing your benefits during this crucial period.

After reviewing your plan with a local licensed agent, there are six possible changes to make:

Are you looking to switch up your Medicare Advantage plan? Every year, from January 1 through March 31, you can make a change during Medicare Advantage Open Enrollment. So mark it on your calendar and take advantage.

During the Medicare Advantage Open Enrollment Period, you’re given a unique opportunity to make any changes or adjustments to your plan. But if this time passes without taking advantage of it, don’t worry – there are still opportunities for change during the Annual and Special Enrollment Periods. Learn more about how these special periods could help shape your coverage today.

Discover the exciting possibilities during the Medicare Advantage Open Enrollment Period. Transform your healthcare experience by making these valuable adjustments:

Discover the flexibility of Special Enrollment Periods (SEPs), designed to accommodate life’s twists and turns. These unique windows open outside the standard enrollment periods, catering to your changing needs and new plan options.

Dive in as we unveil the top three factors that could unlock your access to a Special Enrollment Period.

Moving, losing your health insurance, or the opportunity to get other health insurance could be your ticket to unlocking a Special Enrollment Period. Navigating these uncharted waters can be tricky, so seeking guidance from a local licensed agent is wise. They’ll steer you through the process, pinpoint if you have a qualifying life event, and map out the perfect timeline for your unique situation.

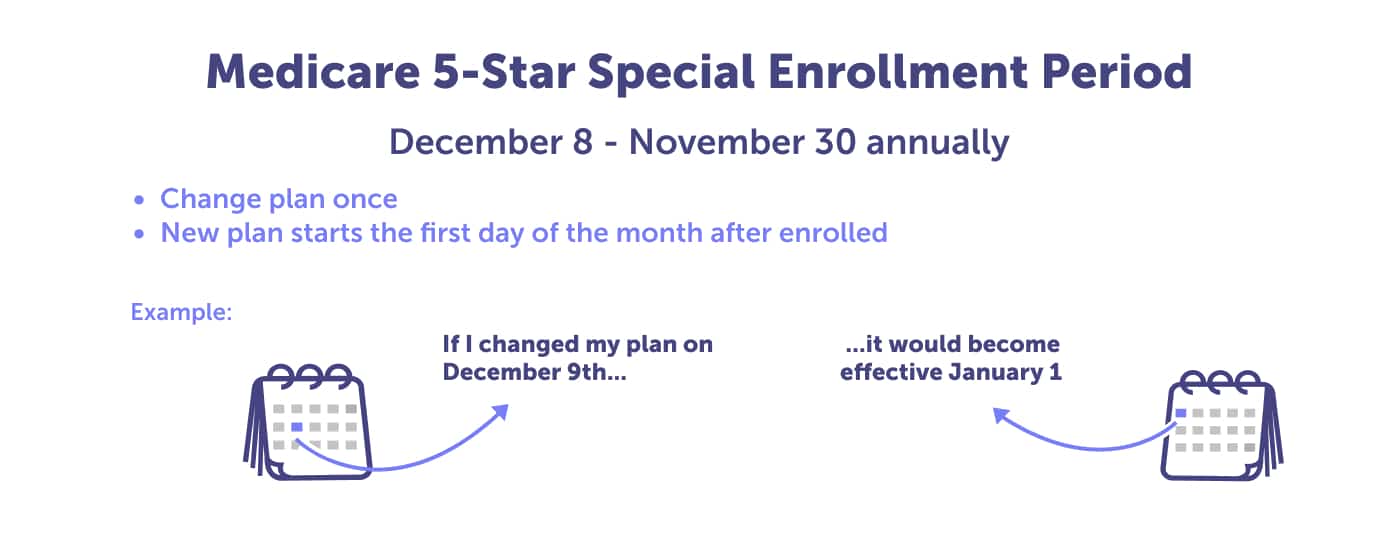

Have you heard of 5-Star Medicare plans? These plans are carefully assessed by the Centers for Medicare & Medicaid Services (CMS), which employ a star rating system to determine the best of the best. Can you guess the highest rating? That’s right – it’s five shining stars.

Want a 5-star rated plan? Use the 5-Star Special Enrollment Period to enroll in a 5-star plan available in your county. During a 5-Star Special Enrollment Period, you can swap your current plan for a top-rated Medicare Advantage, Medicare Advantage Prescription Drug (MAPD) plan, or a stand-alone Medicare Part D prescription drug plan.

The 5-Star Special Enrollment Period can be used once between December 8th and November 30th. Reach out to a local licensed agent for reliable guidance.

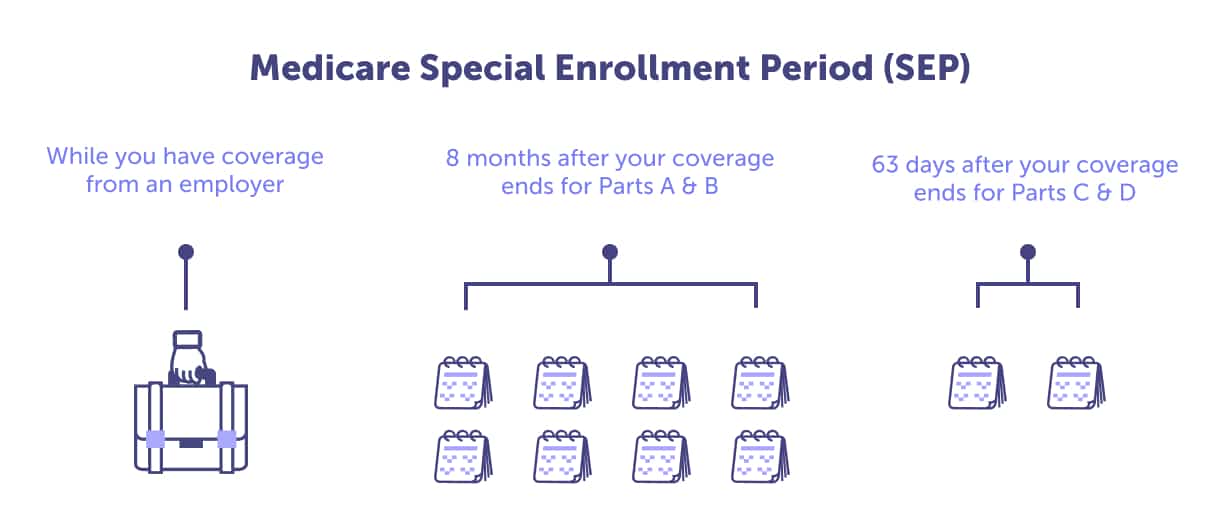

Are you considering delaying Medicare enrollment due to working beyond 65? Ensure that you and your partner’s job-based health insurance matches the quality of Medicare – this is the concept of creditable coverage.

Make a yearly check to ensure you and your spouse safeguard yourselves with adequate Medicare Part B and Part D coverage via your employer. Be cautious about delaying Medicare, as missteps might result in permanent penalties. Verify that you have a dependable alternative source of coverage.

After losing employer-sponsored healthcare, you’ve got eight crucial months to enroll in Medicare Part A and B. Eyeing Medicare Advantage (Part C) or Medicare Part D? Act fast—you’ve got a mere 63 days. Procrastinate and you could face pesky late enrollment penalties. Oh, and just so you know—COBRA won’t save the day here, as it’s not considered creditable coverage.

The Arizona Department of Economic Security offers two programs to assist with Medicare. The State Health Insurance Program (SHIP) helps with enrollment, while the Senior Medicare Patrol (SMP) can aid you in reporting fraud. Both of these programs are offered through Arizona Area Agencies on Aging. You can visit the section below to find the office in your area.

Arizona Department of Economic Security

The Arizona SHIP (State Health Insurance Assistance Program) Program, under the Arizona Department of Economic Security, offers free health benefits and insurance counseling if you’re eligible for Medicare.

Confidential SHIP Program Phone Number: 1-800-432-4040

SHIP Program Resources

AZ Aging is the statewide network of Area Agencies on Aging. They offer various services and programs to improve the quality of life for older adults, people living with disabilities, and their families and caregivers. Services are available throughout Arizona, and you can learn which agency is in your area by visiting the Area Agencies site. These offices also provide SHIP assistance.

Area Agency on Aging (Arizona Aging) Phone Number: 928-298-2574

Local Resources from Area Agency on Aging (Arizona Aging)

The Social Security Administration (SSA) administers retirement and disability income programs for the United States. They provide financial support for retirees. You can apply for retirement, disability, and Medicare benefits through the Social Security Administration.

SSA Phone Number: 1-800-772-1213 (TTY 1-800-325-0778)

Social Security Administration FAQ

Social Security Administration local office locator

Email the Social Security Administration

Working with the Social Security Administration, the Railroad Retirement Board administers the retirement benefits for railroad workers and their families in the United States.

Texas RRB Office Phone Number: 1-877-772-5772

RRB National Telephone Service: 1-877-772-5772

General TTY Number: 1-312-751-4701

Headquarters Personnel Directory: 1-312-751-4300

Railroad Retirement Board website

Arizona Population, 2023.

CMS Releases 2023 Projected Medicare Basic Part D Average Premium.

MA State/County Penetration, February 2023.

Medicare Advantage in 2022: Enrollment Update and Key Trends.

Medicare Costs.

Medicare Open Enrollment in Arizona, 2022.

Medicare Open Enrollment in Arizona, 2023.

The State of Medicare Supplement Coverage, 2020.

Total Number of Medicare Beneficiaries by Type of Coverage, Arizona.

What Medicare Part D drug plans cover.

What Part B covers.

Yearly deductible for drug plans.

Last updated: May 1, 2023

Medicare typically does not cover assisted living in Arizona. You and your family usually pay for the out-of-pocket costs to cover assisted living. Long-term care insurance can also help pay for the cost.

Read more about whether Medicare covers assisted living.

You can apply to Medicare in Arizona by contacting a Connie Health local licensed agent. Call 1-888-647-7330 to have an advocate support you from the beginning of your Medicare journey. You can also contact the Social Security Administration to apply for Medicare.

Learn more about your plan options and how to apply for Medicare in Arizona.

The Mayo Clinic may accept those enrolled in Original Medicare Parts A & B and Medicare Supplement (Medigap) plans.

The Mayo Clinic does not require doctor referrals, but you may need preauthorization. Medicare is not accepted for primary care services, and they do not accept Medicare Advantage plans. The only exception is in the event of an emergency.

Read more about whether the Mayo Clinic accepts Medicare.

You’ll likely enroll in Original Medicare Parts A and B in Arizona. Most Arizona Medicare beneficiaries then decide to enroll in a Medicare Advantage or Supplement plan to shield themselves from the high out-of-pocket costs of Original Medicare.

At the same time, you’ll need to choose how to get creditable prescription drug coverage, which the Centers for Medicare & Medicaid Services (CMS) requires. You can speak to a local licensed agent in Arizona by calling 1-888-647-7330 or learning more about Arizona Medicare plans.

There isn’t a best or one-size-fits-all Medicare Advantage plan in Arizona. Your chosen plan should be based on your unique health and budget needs. There’s a lot to weigh, and you shouldn’t base your decision on what plan your neighbor or spouse is enrolled in – or the most popular plan.

For more on choosing a Medicare Advantage plan in Arizona or help with choosing, call 1-888-647-7330 or visit Medicare Advantage Plans in Arizona.

While there isn’t a best option, the most popular plan options in Arizona are Plan F, Plan G, Plan N, and Plan C. Unfortunately, if you turned 65 after January 1, 2020, Plan F and Plan C will not be available to you – they have been phased out. Enrollment in Plan G is increasing – it’s the closest to popular Plan F.

Remember that when making a Medicare Supplement plan choice, it should be tailored to your health and budget needs. Even though these are the most popular plans doesn’t mean any of them are the best for you. Instead, compare plans and consider additional benefits such as discounts on prescriptions or vision care services that may save you money.

If you need help deciding on the best Medicare Supplement plan, call an Arizona local licensed agent at 1-888-647-7330 or read more at Medicare Supplement Plans in Arizona.

Yes, you can get Medicaid and Medicare in Arizona. People who are enrolled in both are called “dual eligible.”

Medicare will pay first when you’re dual eligible and you get Medicare-covered services. Medicaid pays after Medicare and any other health insurance plan you may have. The Arizona dual-eligible program is operated by the Arizona Health Care Cost Containment System (AHCCCS).

If you need help enrolling in Medicare and Medicaid, contact a Connie Health local licensed agent who can help. Call 1-888-647-7330.

Discover your Arizona Medicare plan options (Parts A, B, C, D, and Medicare Supplement) and how to avoid late enrollment penalties.

Curious about Medicare Advantage plans in Arizona? Learn about their costs and coverage, choosing the right plan for you, and when to enroll.

Original Medicare does not cap expenses. Learn how a Medicare Supplement Plan in Arizona could help with some or all of those costs.