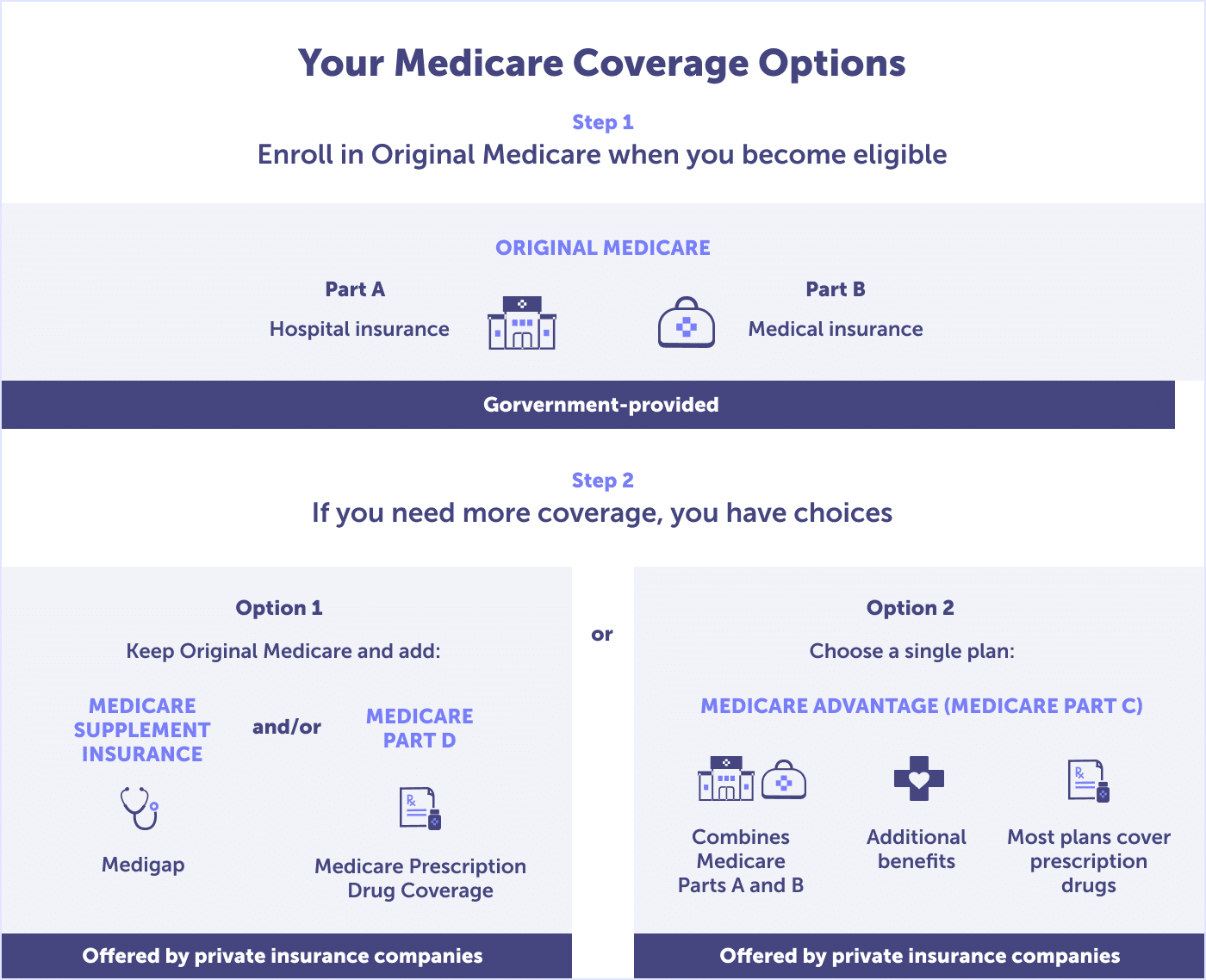

A Medicare Advantage plan is an alternative way to receive Original Medicare in Florida, with extra benefits. Also referred to as Medicare Part C, Medicare Advantage plans are offered by private insurance companies that contract with the Centers for Medicare & Medicaid Services (CMS). Approximately 55% of Floridians are enrolled in a Medicare Advantage plan in 2026.

To enroll in a Medicare Advantage plan, you must be enrolled in Medicare Part A (hospital insurance) and Medicare Part B (medical insurance) and live in the plan’s service area. Medicare Advantage plans are local—to the county level—and have many options for you to choose from.

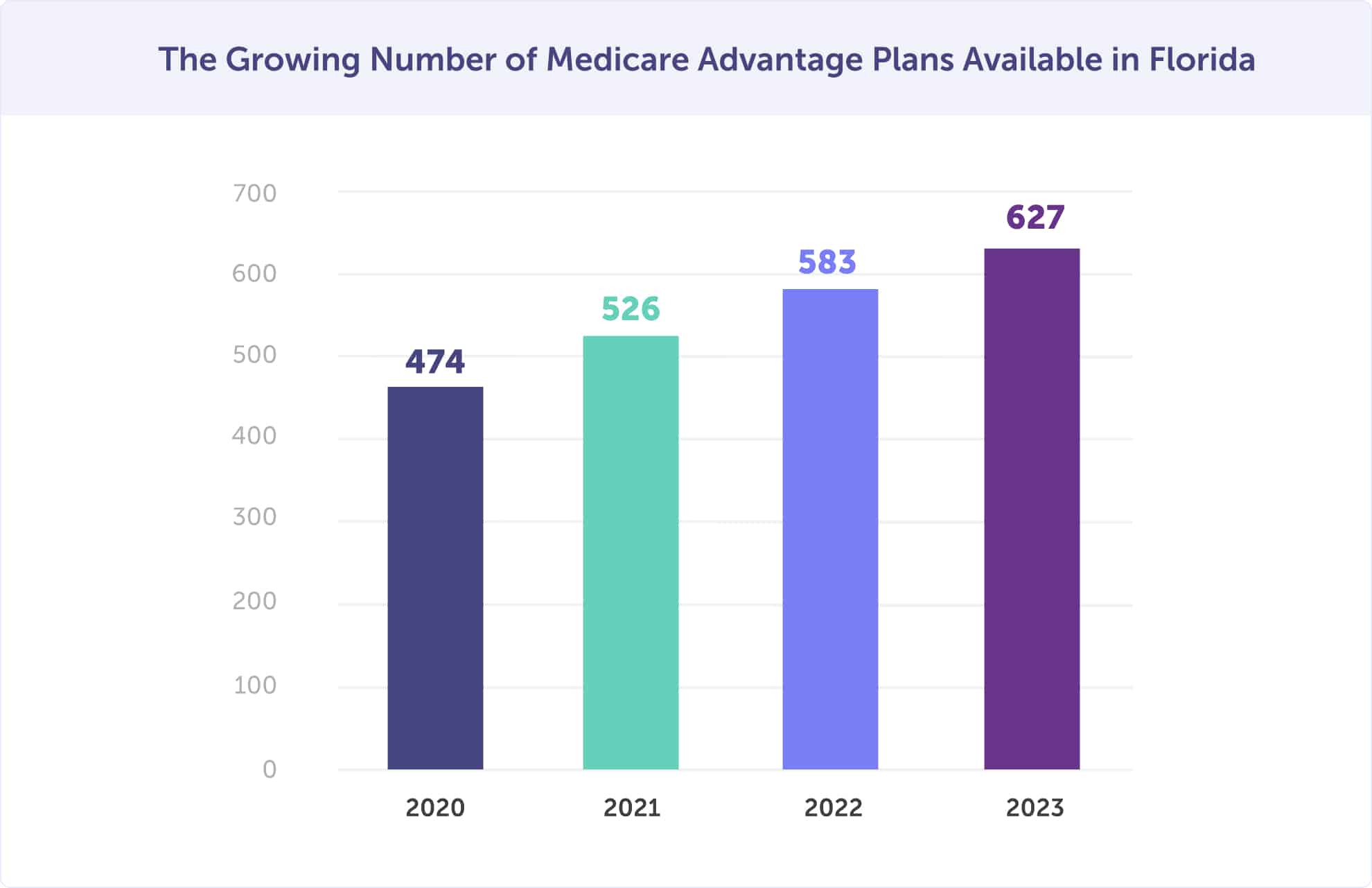

In Florida, there are 627 Medicare Advantage plans available in 2026. That’s a 7.5% increase when compared to the 583 Medicare Advantage plans available in 2022. There were 526 plans available in 2021 and 474 plans available in 2020.

Now, you have an even greater opportunity to find a suitable plan for your health and budget.

And most of these plans offer enrollees routine dental, hearing, and vision, plus innovative benefits such as wellness and healthcare planning, reduced cost-sharing, and rewards and incentives programs. These are benefits that Original Medicare does not offer.

The 10 Florida counties with the highest Medicare Advantage enrollment are Miami-Dade County (75%), Osceola County (70%), Gadsden County (68%), Pasco County (66%), Polk County (65%), Hernando County (65%), Liberty County (64%), Broward County (64%), Wakulla County (62%), and Calhoun County (60%).

The counties that saw the largest percentage increase in enrollment between 2022 and 2023 are Gadsden County, Pasco County, Hernando County, and Liberty County. Each of these counties increased by 2% year-over-year.

Medicare Advantage plans must provide the same coverage as Original Medicare Part A and Medicare Part B. These plans also usually offer prescription drug coverage (Part D) and are called Medicare Advantage Prescription Drug (MAPD) plans. Some plans include additional benefits not covered by Original Medicare – such as dental, vision, hearing, and more.

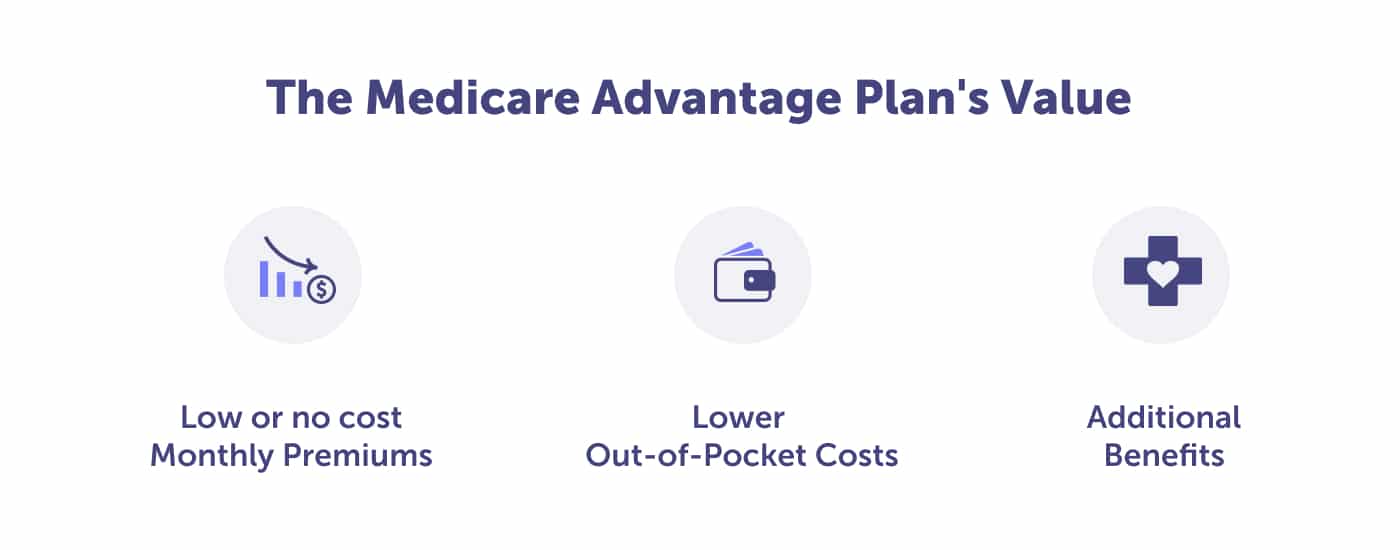

A Medicare Advantage plan can offer you low or no premiums, and lower out-of-pocket expenses, with additional benefits that Original Medicare doesn’t provide. A Medicare Advantage plan offers the coverage of Original Medicare Parts A and B in Florida, but often at a lower cost.

100 percent of people enrolled in Medicare in Florida have access to a $0 monthly premium Medicare Advantage plan. In 2026, the average monthly premium for a Medicare Advantage plan is $9.41. If you enroll in a Medicare Advantage plan in Florida, you’ll pay the Medicare Advantage premium and the monthly Medicare Part B premium.

The bonus of Medicare Advantage? Most plans include prescription drug coverage, and unlike Original Medicare, there is an out-of-pocket maximum.

Original Medicare Parts A and B do not have a maximum for what you spend on copayments or coinsurance, but Medicare Advantage plans do. Medicare Advantage plans set their deductibles, coinsurance, and copays within limits established by the federal government.

Once you reach your plan’s out-of-pocket maximum, including the deductible, your Medicare Advantage plan pays 100% of covered healthcare expenses for the remainder of the plan year.

If you’d prefer to keep Original Medicare (Parts A & B) but want more predictable out-of-pocket costs, a Medicare Supplement plan in Florida (Medigap) is an alternative to Medicare Advantage. If you choose a Medicare Supplement plan, the monthly premium may be higher, and you’d likely need to sign up for Medicare Part D to have creditable prescription drug coverage.

Not sure if a Medicare Advantage or Medicare Supplement is best for your health and budget? Compare plans online or call to speak with a local licensed agent to help narrow your choices. Call (623) 223-8884.

Original Medicare doesn’t provide coverage for dental, hearing, or vision. These are additional benefits that most Medicare Advantage plans offer. And most plans also include reduced cost-sharing, over-the-counter and wellness products, transportation assistance, telemedicine, fitness programs, and other rewards and incentive programs.

In 2026, the Centers for Medicare & Medicaid Services (CMS) Value-Based Insurance Design (VBDI) program offers Florida enrollees two unique programs.

Through the CMS Innovation Center, 210 Medicare Advantage plans offer enrollees:

Through the Value-Based Design Insurance Model’s Hospice Benefit Component, 1 plan(s) offers the Medicare hospice benefit through their plan.

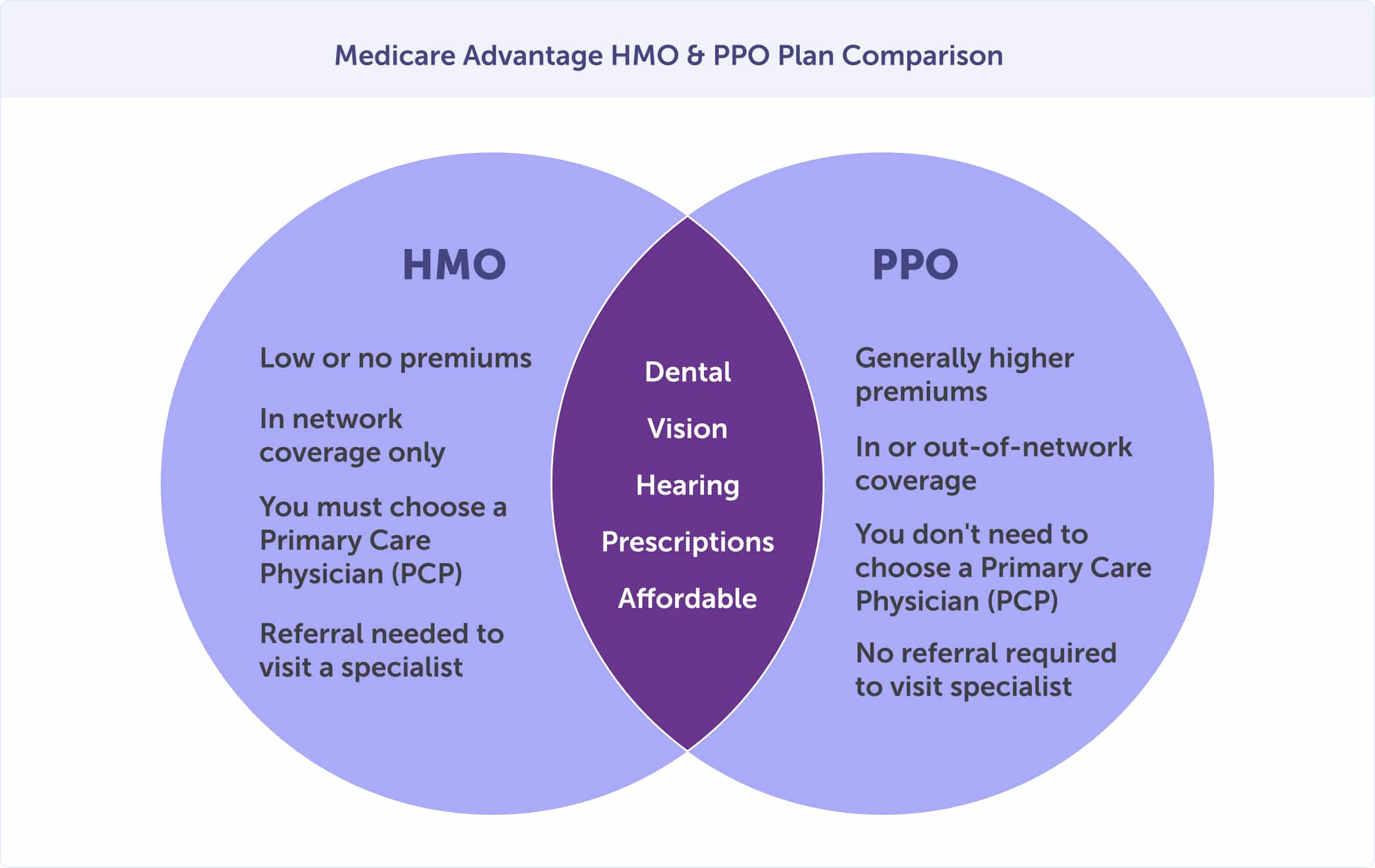

There are four types of Medicare Advantage health plans for you to choose from. The two most common types are Health Maintenance Organizations (HMOs) and Preferred Provider Organizations (PPOs). The lesser utilized plans are Special Needs Plans (SNPs) and Private Fee-for-Service (PFFS). Likely, a PFFS plan is not available in your area unless you live somewhere especially rural.

What do all the plans have in common?

Each plan type provides a different level of network flexibility and price. However, all Medicare Advantage plans are required to provide the same coverage as Medicare Part A and B. Continue reading to learn about what each plan type offers – and to find the one that’s the right fit for you.

Agent tip:

“When choosing amongst your Medicare Advantage plan types, you’ll be making a decision between coverage, flexibility, and cost. If you have a special need, a SNP plan would be a good choice. If you want maximum network flexibility, a PPO. But if you want to reduce costs, an HMO is the way to go.“

Health Maintenance Organization (HMO) plans are the most popular Medicare Advantage plan for enrollees. These plans usually require that you receive all services in a network.

If your goal is to maintain your existing relationships with doctors, hospitals, or other care providers, check if your preferred healthcare providers participate in a Medicare Advantage plan’s network.

Do you need help picking a plan that includes the doctors you value and the prescriptions you need? Call Connie Health to find a plan that maintains your doctors: (623) 223-8884.

Preferred Provider Organization (PPO) plans have a network of preferred providers, but you can choose doctors or hospitals from outside of the network at a higher cost. You can typically choose between regional or local PPO providers.

Special Needs Plans (SNPs) limit membership to people with specific diseases or characteristics. These plans are tailored to meet the particular needs of the service groups, including provider choices and drug coverage.

Private Fee-for-Service (PFFS) plans determine how much it will pay doctors, health care providers, and hospitals and how much you must pay when you receive care. With this plan, you pay any cost-sharing expenses at the time of service. After that, the provider bills your plan for the remaining amount.

The lowest premium for a Medicare Advantage plan is $0. And 100 percent of people with Medicare Part A and B have access to a Medicare Advantage plan in Florida with a $0 monthly premium. However, the average monthly premium in 2026, for those who have one, is $9.41.

When you enroll in a Medicare Advantage or MAPD plan, premiums are paid directly to the plan provider. Your Medicare Part B premium is paid directly to Medicare, traditionally withdrawn from your Social Security benefit – or paid monthly or quarterly.

In addition to the premium, out-of-pocket expenses will need to be paid. These include deductibles, copayments, and coinsurance. The costs depend on which plan you choose.

Check if you qualify for a $0 premium Medicare Advantage plan. Call (623) 223-8884 to speak with a local licensed agent today.

When considering your plan options, you’ll be weighing coverage and cost. Here are a few questions to ask while shopping for the right plan for your health and budget.

Enter your doctors and prescriptions into Connie Health’s Medicare plan finder, and we’ll narrow your plan options. Or call (623) 223-8884 to speak with a local licensed agent.

Knowing when you should enroll or when you can make a Medicare Advantage plan change could save you money. Continue reading to learn about one-time enrollment periods you don’t want to miss and when you can make changes. Get ready to mark your calendars.

The Initial Enrollment Period is the seven-month window when most Floridians enroll in Medicare Part A and B. This enrollment period begins three months before you turn 65, includes the month of your birthday, and ends three months after you turn 65.

If you’re not collecting Social Security benefits by the time you reach your Initial Enrollment Period, you’ll need to sign up for Medicare. If you don’t enroll in Medicare Part B during your Initial Enrollment Period, you could incur a lifetime late enrollment penalty. This amount is added to your standard Part B premium, increases the longer you wait, and is never removed.

If you miss your Initial Enrollment Period, you may be able to enroll during the General Enrollment Period or a Special Enrollment Period if you qualify.

Not sure when your Initial Enrollment Period is? Call (623) 223-8884 to speak with a local licensed agent and avoid late enrollment penalties.

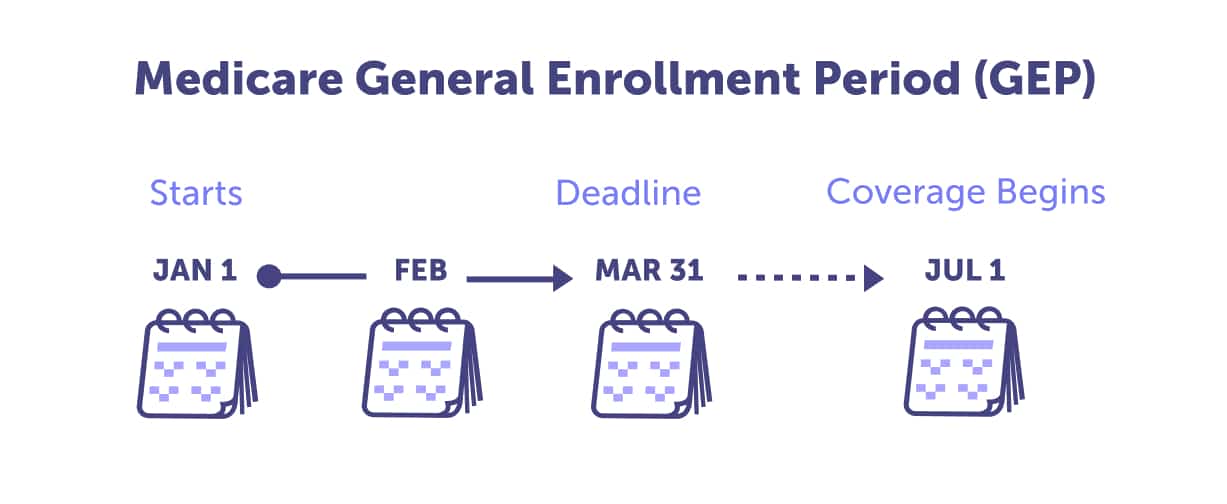

If you miss your Initial Enrollment Period, you should mark Medicare’s General Enrollment Period (GEP) on your calendar. This enrollment period starts on January 1, annually, through March 31. If you enroll in Medicare Part A and B or make a plan change during the General Enrollment Period, coverage will begin on July 1st.

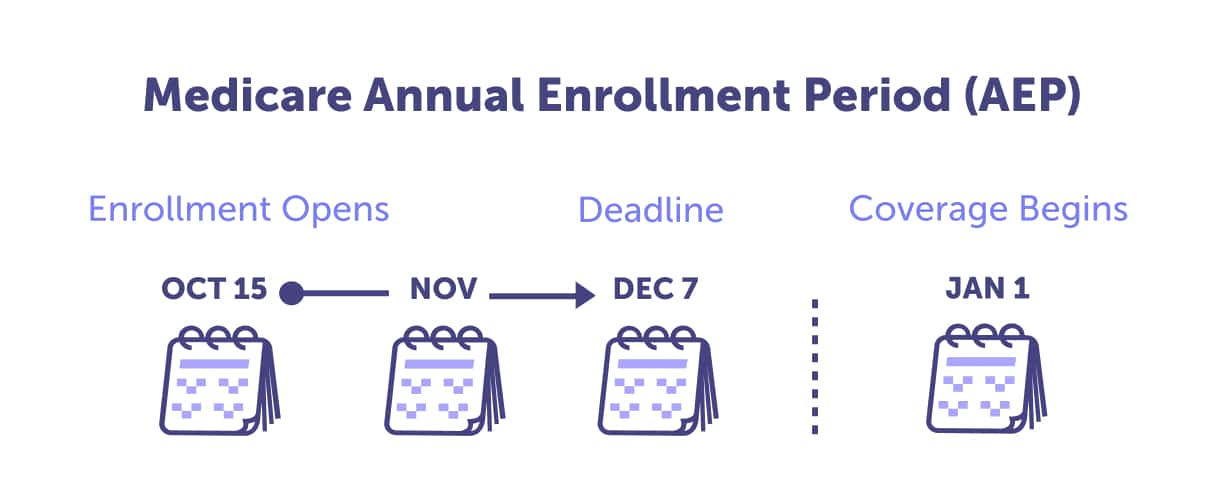

The Annual Enrollment Period (AEP) is for individuals already enrolled in Medicare Part A and B and who want to change their plan. The Medicare Annual Enrollment Period happens every year between October 15 and December 7.

You can make several plan changes during this time, including switching from Original Medicare to a Medicare Advantage plan, with or without prescription drug coverage. You can also switch to another Medicare Advantage plan, among other plan change options. Read our Ultimate Guide: The Medicare Annual Enrollment Period to learn how to prepare for this crucial enrollment period.

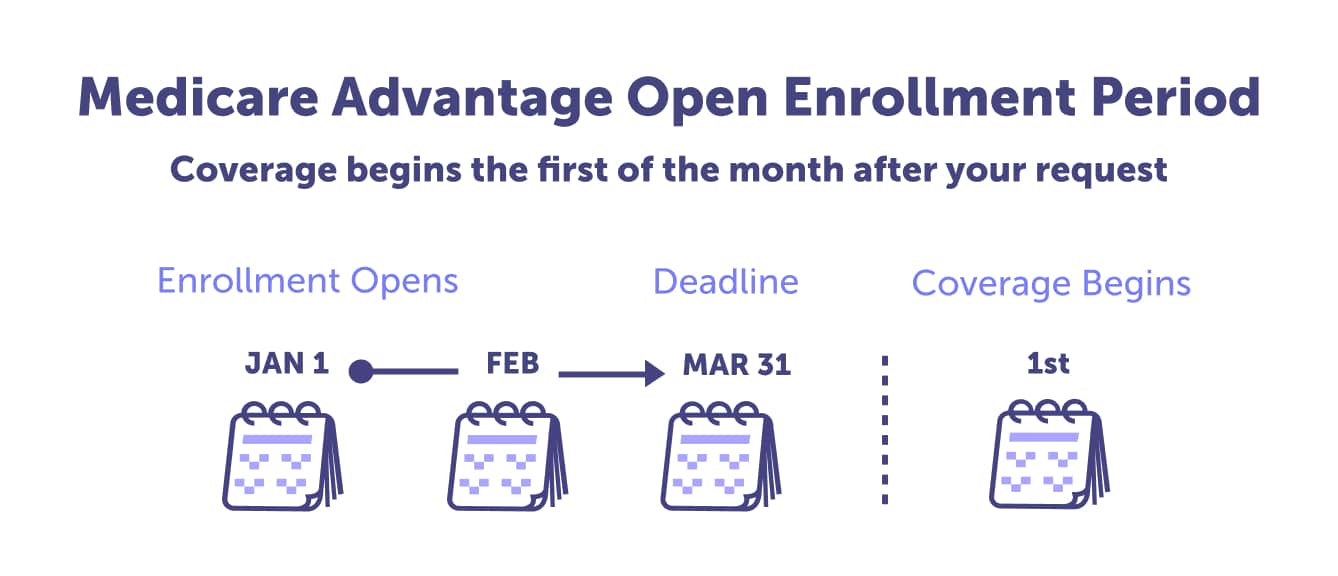

The Medicare Advantage Open Enrollment Period (MAOEP) is for individuals enrolled in a Medicare Advantage plan. This enrollment period occurs annually between January 1 through March 31st.

It’s during this time that you can make a one-time plan change. There are three plan changes that you cannot make:

If you’d like to switch to another Medicare Advantage plan, with or without prescription drug coverage, or go back to Original Medicare – these are all options.

Not happy with your Medicare Advantage plan? Call (623) 223-8884 and speak to a local licensed agent to discover the best enrollment period to make a change.

There are certain instances when you qualify for a Special Enrollment Period (SEP) and can make a plan change. These include if you move out of your plan’s services area, lose your current coverage, or have the chance to get other coverage, among other reasons. If you qualify for a Medicare Special Enrollment Period, you’ll have the opportunity to sign up for or make Medicare Advantage or Medicare Advantage Prescription Drug plan changes.

Have a local licensed agent review your enrollment periods and plan options in Florida. Call (623) 223-8884 to speak with an agent or review plan options online.

MA State/County Penetration – February 2023.

MA Landscape Source File, 2023.

Medicare Open Enrollment in Florida, 2022.

Medicare Open Enrollment in Florida, 2023.

Last updated: March 3, 2023

The best Medicare Advantage plan in Florida is the one that is best for your unique health and budget needs. There are, however, Medicare insurance providers who are popular with enrollees in Florida. The top 5 providers are Humana, UnitedHealthcare, Aetna, BlueCross BlueShield, and Sunshine State Health Plan. You may want to consider one of these companies when making your decision.

The highest-rated Medicare Advantage plans in Florida are five-star rated plans. When a plan receives a 5-star rating, it is ‘excellent,’ according to the rating system established by the Centers for Medicare and Medicaid Services (CMS).

The number of 5-star Medicare Advantage plans in Florida varies by county. The highest-rated plans offer high-quality care and patient satisfaction, among other factors.

Plans are evaluated annually on how well the plan works to prevent hospitalizations, how often members receive certain screenings and vaccinations, and how well chronic conditions like diabetes or heart disease are managed. CMS also surveys enrollees about the plan’s customer service, how easy it is to get appointments, and whether they would recommend the plan.

Read more by William Revuelta

I am a Spanish-speaking Florida Life and Health Insurance Licensed Agent and have been helping people with Medicare since 2009. I’m an avid sports fan and enjoy watching international soccer matches and college football. When not with my family, I listen to podcasts ranging from history to sports talk.